Introduction: The Critical Balance of the Modern Grid

The electrical grid operates under a physical constraint unique among commodity markets: at every millisecond, generation must precisely match consumption. Historically, this equilibrium was maintained via dispatchable generation — coal, gas, and hydro units that could modulate output in response to demand. However, the global energy transition has dismantled these traditional management assumptions. As we pivot toward weather-dependent, variable renewable energy (VRE), supply is no longer a controllable variable but an exogenous one. In this paradigm, Energy Storage Systems (ESS) have evolved from a non-ancillary supplemental resource into a foundational infrastructure requirement for grid survival.

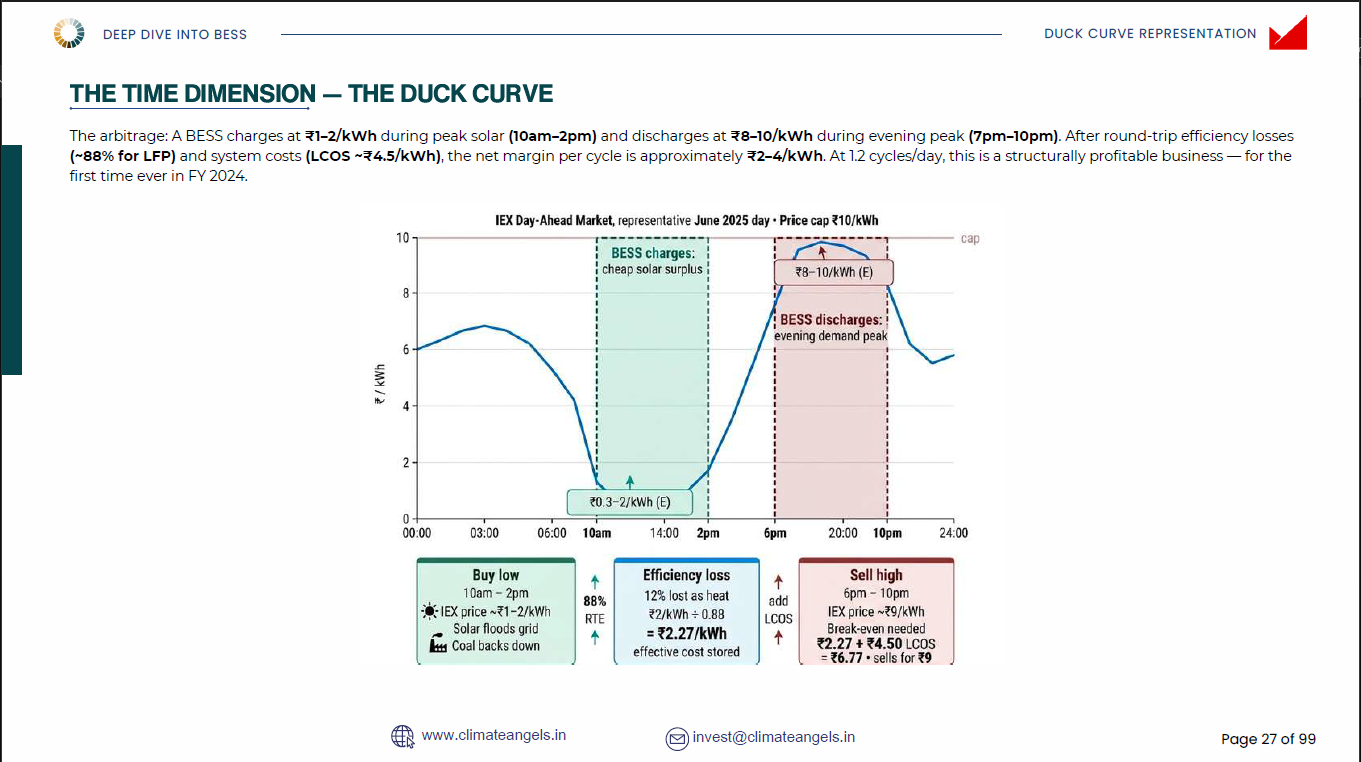

In India, this transition is best illustrated by the “Duck Curve.” The grid now experiences a massive midday surplus of low-marginal-cost solar energy, driving market prices on the IEX Day-Ahead Market to collapse — regularly hitting ₹0.30/kWh. Conversely, as solar output drops, residential and commercial demand surges for the evening peak, pushing prices toward the ₹10/kWh regulatory ceiling. This midday-to-evening spread has widened at a 17% compound annual growth rate since 2019, creating a structural arbitrage opportunity. Battery Energy Storage Systems (BESS) are the primary technological solution to this temporal mismatch, providing the flexibility necessary to stabilize a high-penetration renewable grid.

Decoding BESS: The Technical Language of Storage

For the strategic investor, a BESS asset is not merely a piece of equipment but a complex financial instrument governed by electrochemical physics. Understanding technical specifications is mandatory, as these metrics directly dictate the asset’s ability to capture specific revenue streams. For instance, response times determine eligibility for high-value ancillary services, while cycle life dictates the long-term capital expenditure required for battery augmentation.

The report synthesizes the core concepts essential for evaluating the financial viability of storage projects — from the distinction between power and energy ratings to round-trip efficiency, depth of discharge, and levelized cost of storage.

Strategic Asset Allocation Implications. The distinction between MW (Power) and MWh (Energy) defines the asset’s role in a portfolio. MW-heavy systems are designed for sub-second stabilization, earning high premiums for speed, while MWh-dense assets are designed for energy-shifting over several hours. An investor must align the technical configuration of the BESS with the intended market: 2-hour systems are currently the commercial “sweet spot” for capturing India’s peak spreads and providing grid services, while 4-hour systems are increasingly required by the National Electricity Plan (NEP-14) to provide firm renewable capacity.

Beyond Arbitrage: The Multi-Dimensional Value of BESS

While price arbitrage is the most visible revenue driver, BESS provides a suite of critical grid services essential for replacing the “spinning reserve” and “governor response” of retiring thermal assets. BESS outperforms traditional thermal “peaker” plants across four critical dimensions:

Frequency Regulation: As the grid loses the natural inertia of coal plants, BESS provides primary frequency response. These assets can respond in under 30 milliseconds — orders of magnitude faster than thermal ramping. Under India’s Secondary Reserve Ancillary Services (SRAS), operators can capture revenue by maintaining dispatch accuracy exceeding 95%.

Spinning Reserve: BESS provides instantaneous capacity to cover sudden generation losses. Unlike coal plants, which must burn fuel while idling to provide this service, batteries maintain readiness with zero fuel consumption and minimal mechanical wear.

Black Start Capability: In the event of system failure, BESS can re-energize grid segments without external power. As coal assets retire, this capability serves as a vital, non-negotiable insurance policy for national grid resilience.

Transmission Congestion Management: By absorbing local surpluses, BESS can defer or eliminate the need for transmission upgrades costing hundreds of crore per kilometer. Under CERC frameworks, this “grid deferral value” provides uncorrelated diversification, as revenue is independent of wholesale price volatility.

The India Context: A 236 GWh Strategic Necessity

India’s storage mandate is driven by the aggressive target of 500 GW of non-fossil capacity by 2030. To maintain grid stability at this scale, the National Electricity Plan requires 236 GWh of storage. Without this infrastructure, the grid faces massive “curtailment” — the economically perverse practice of switching off solar generation because it cannot be absorbed.

India-Specific Strategic Drivers

Deployment Velocity: India is adding renewable capacity faster relative to GDP than any other major economy, creating an immediate, acute need for flexibility.

Thermal Fleet Inflexibility: Much of India’s coal fleet consists of large supercritical units that cannot ramp down below 55–65% of rated capacity without risking damage, leaving the grid unable to accommodate solar peaks.

Industrial Scale: With over 600,000 MW of industrial load, there is a massive opportunity for behind-the-meter storage. Industrial consumers face peak tariffs of ₹8–12/kWh, creating a strong internal rate of return (IRR) for on-site storage that avoids high demand charges.

The Investment Landscape: Risks, Barriers, and Realities

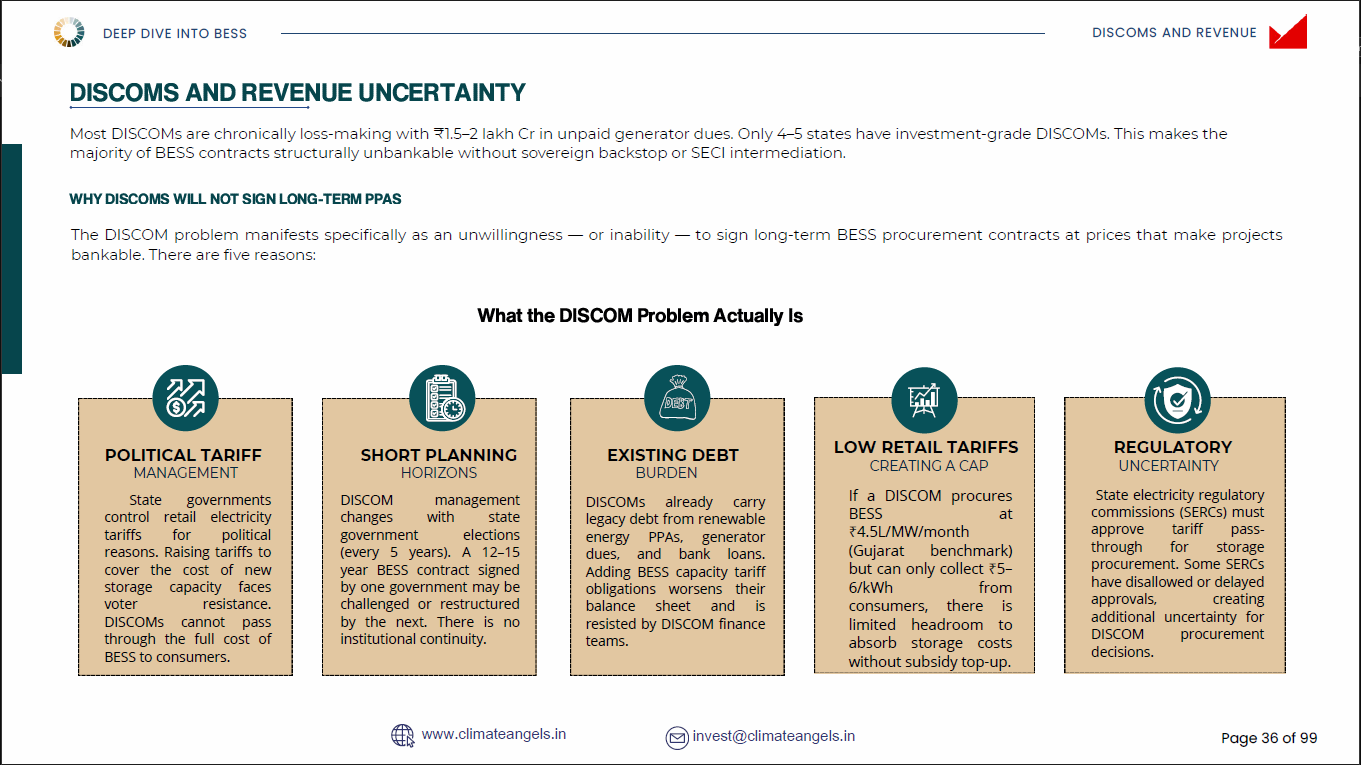

The transition from policy aspiration to a bankable reality is currently obstructed by institutional chokepoints that investors must carefully navigate. Two critical risks dominate the current bankability agenda:

DISCOM Financial Health: The persistent financial weakness and payment unreliability of India’s distribution companies (DISCOMs) remain the primary bottleneck. For BESS projects to be bankable, they require a solvent, reliable offtaker to sign long-term capacity contracts.

Supply Chain Vulnerability: Approximately 85% of global Lithium Iron Phosphate (LFP) cell production is controlled by China. Every megawatt deployed in India today deepens this strategic dependency, as domestic cell manufacturing has yet to reach meaningful commercial scale.

The Analyst’s Perspective on Returns. Merchant arbitrage economics only crossed the threshold of viability in FY2024. While the widening Duck Curve makes the case for energy shifting compelling, the most robust investment cases now incorporate secondary revenue streams like SRAS (yielding roughly ₹0.50/kWh for high-accuracy dispatch). Successful BESS portfolios will be those that balance merchant volatility with grid services to achieve uncorrelated, risk-adjusted returns.

Conclusion: Unlocking the Future of Energy

BESS is the only technology capable of profitably bridging the gap between midday solar abundance and evening demand surges. It is the linchpin of India’s energy transition. However, realizing the sector’s potential requires moving beyond technology pilots to address the “bankability agenda” — ensuring fiscal solvency among offtakers and diversifying revenue streams.

As the grid moves toward a 100x acceleration in capacity, the opportunity for early movers to capture structural arbitrage and provide essential grid services is unprecedented.

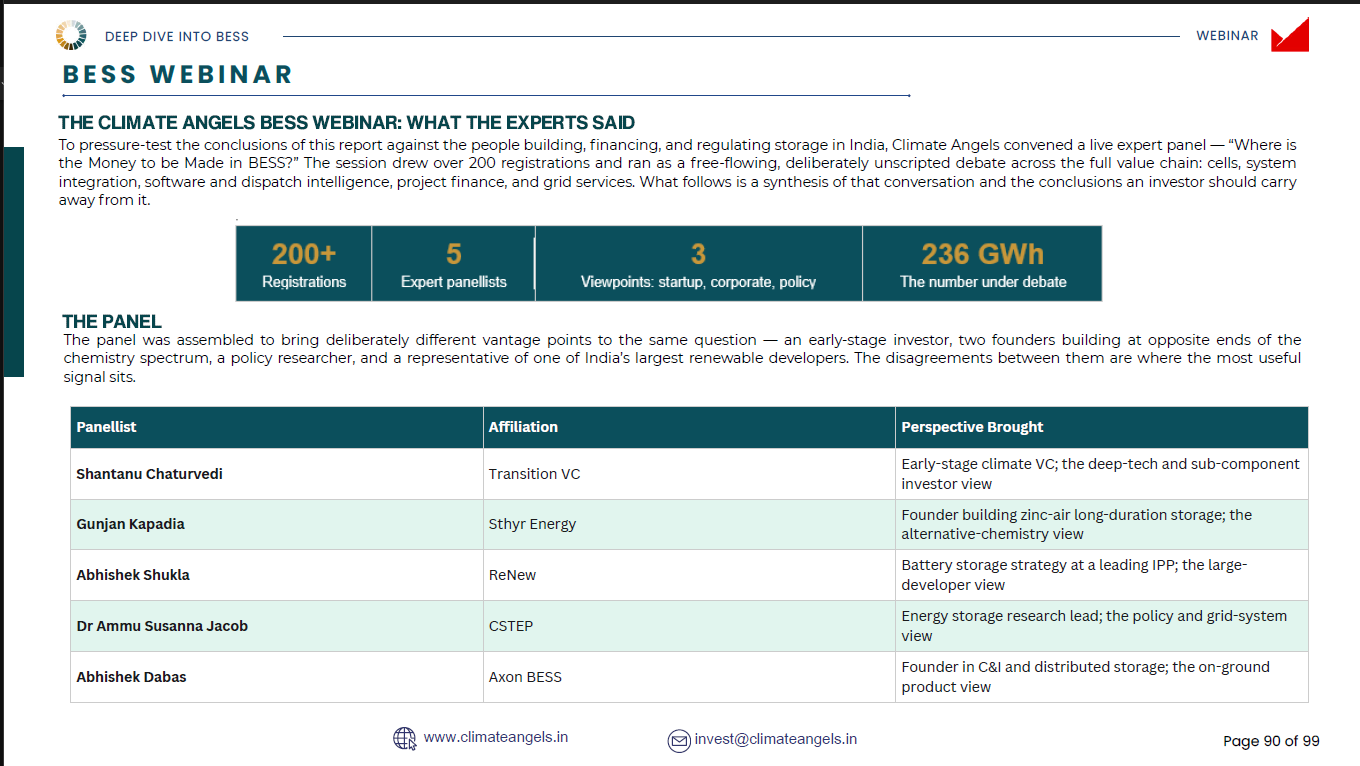

The Climate Angels BESS Webinar: What the Experts Said

To pressure-test the conclusions of this report against the people building, financing, and regulating storage in India, Climate Angels convened a live expert panel — “Where is the Money to be Made in BESS?” The session drew over 200 registrations and ran as a free-flowing, deliberately unscripted debate across the full value chain: cells, system integration, software and dispatch intelligence, project finance, and grid services.

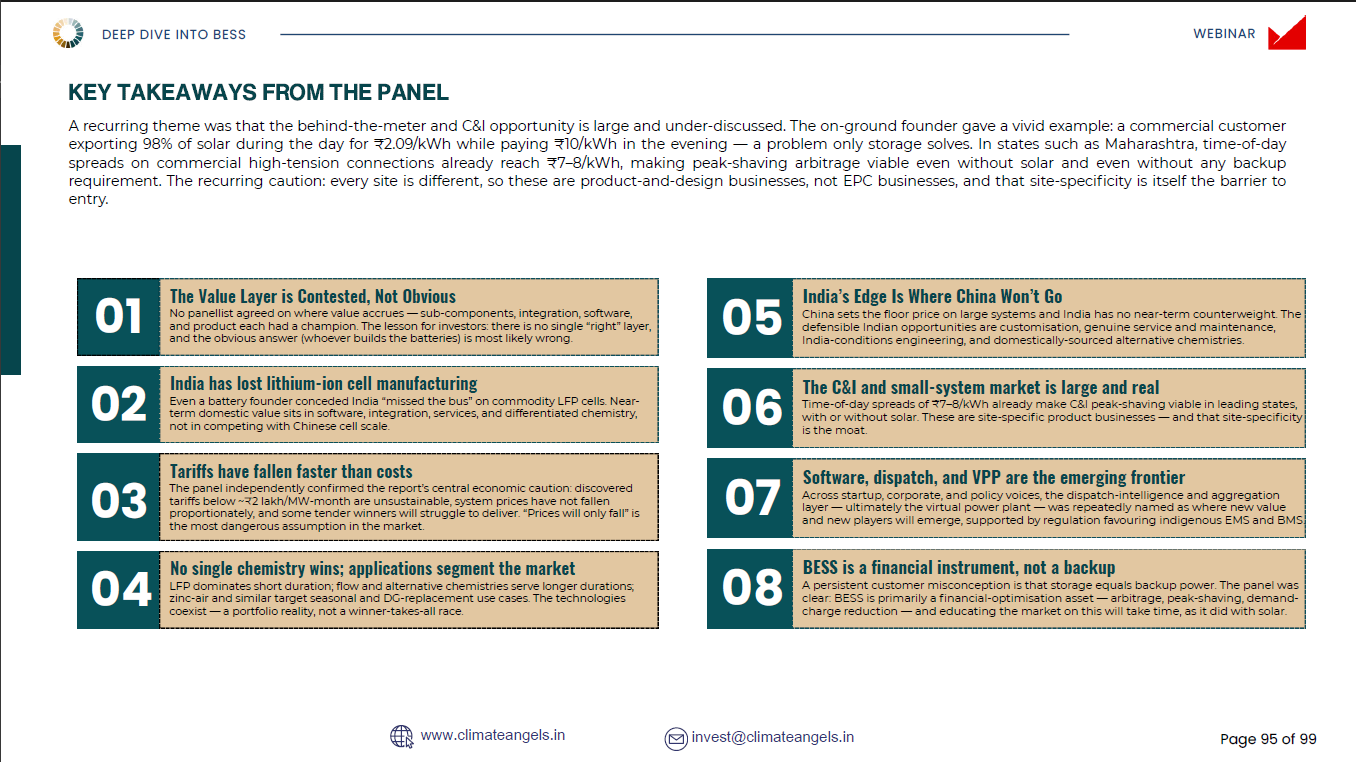

“Everyone assumes BESS prices will only go down. That is the worst assumption one can make.”

— Abhishek Shukla, ReNew